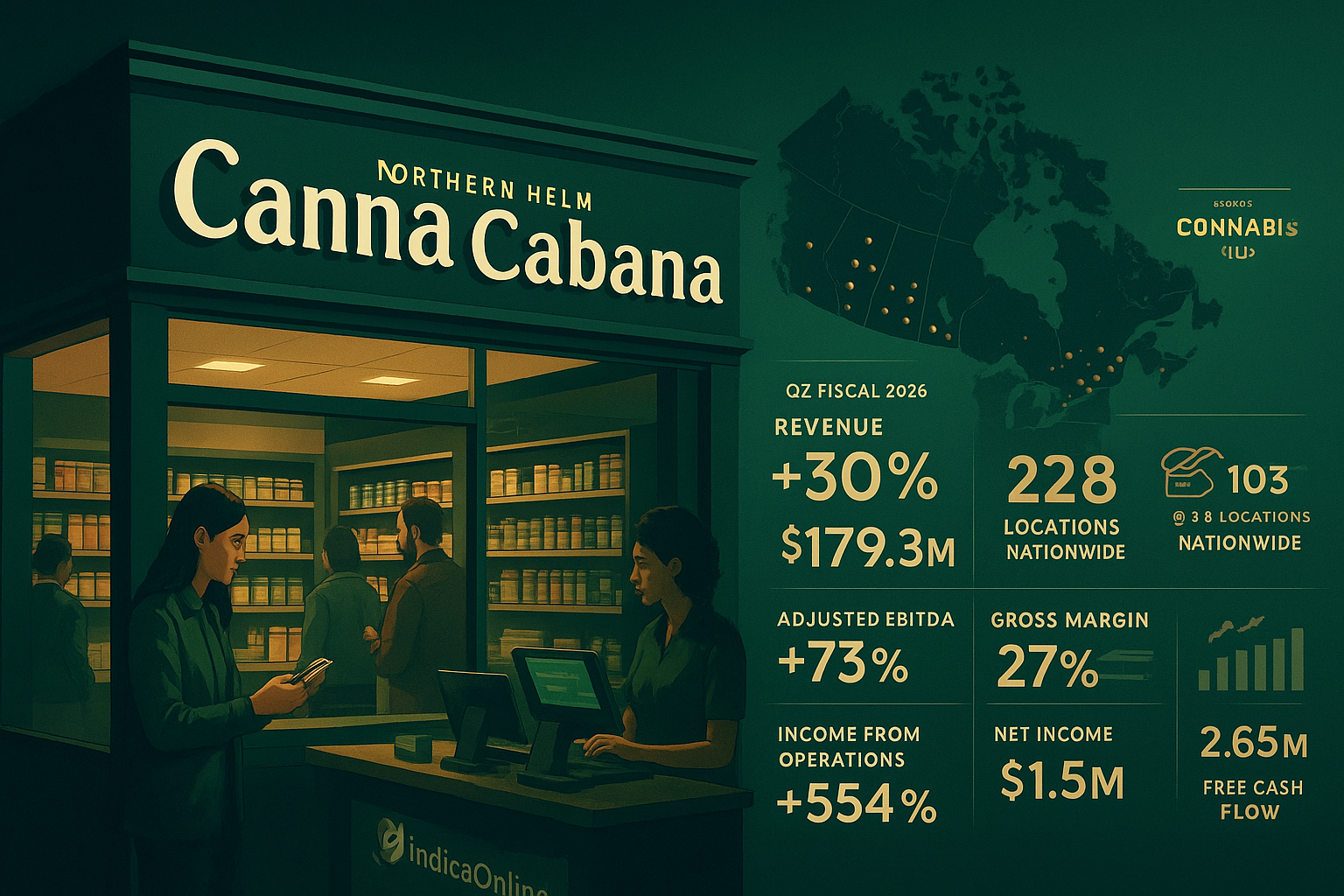

High Tide Inc. reported record second-quarter fiscal 2026 results this month, with revenue climbing 30% year over year to $179.3 million and adjusted EBITDA rising 73% to $13.9 million - numbers that put Canada's largest cannabis retailer in a category few publicly traded cannabis operators have managed to reach: consistent, measurable profitability. The same day those results dropped, the company announced a $7.74 million deal to acquire four Ontario cannabis retail stores operating as Northern Helm, pushing its Canna Cabana network toward 228 locations nationwide. For operators watching the consolidation trend in licensed Canadian cannabis retail, this is worth paying attention to.

The Northern Helm deal is structured as a mix of assumed debt (roughly $3.2 million), cash (about $1.83 million), and High Tide common shares (approximately $2.75 million), priced at 4.5x annualized adjusted EBITDA - a multiple that reflects both the current valuation environment for single-operator cannabis retail assets and the strategic premium High Tide places on Ontario market density. Ontario, with its large adult-use consumer base and retail license expansion since 2020, has become the most competitive provincial market in Canada. Reaching 103 stores there through this acquisition isn't a vanity number; it represents real shelf-presence and supply chain leverage in a market where wholesale pricing and product availability are tied directly to volume. Operators running smaller multi-store groups who rely on a system like IndicaOnline cannabis POS to manage inventory, compliance logs, and sales reporting across locations will recognize the operational complexity that comes with each new store added to a network - and why scale matters for managing that complexity cost-effectively.

What's striking about High Tide's financials isn't just the top-line growth. Gross margin improving to 27% - up from the prior-year period - signals better cost discipline across the retail operation. Income from operations rising 554% to $6.1 million is the kind of number that separates a retailer building a real business from one running on equity raises and deferred losses. The company also reported positive net income and $1.5 million in free cash flow. In an industry where 280E-equivalent tax burdens and excise duties routinely compress operator margins, generating free cash flow at retail scale is not something every cannabis retailer can claim.

Membership Programs as a Retention Tool - and a Data Asset

Cabana Club membership crossing 2.65 million is worth unpacking beyond the marketing headline. In licensed cannabis retail, a large opt-in membership base functions as more than a loyalty program - it produces purchase-pattern data that operators can use to inform wholesale buying decisions, SKU management, and promotional cadence. Regulated markets restrict cannabis advertising in ways that make in-store loyalty programs one of the few compliant customer retention tools available. High Tide has built that asset at a scale most independent dispensaries and smaller multi-store groups simply cannot replicate.

The Canna Cabana store format operates on a discount retail model, which creates its own set of operational pressures. Discount-driven volume requires tight inventory management, disciplined shrinkage controls, and a wholesale buying strategy that keeps cost-of-goods low enough to sustain margin while still meeting provincial excise obligations. The 36% year-over-year increase in gross profit - outpacing revenue growth - suggests the company is executing that balance reasonably well. Whether that margin profile holds as the company absorbs new store locations, including the Northern Helm assets, will be the more telling metric to watch in coming quarters.

Consolidation Pressure on Independent Operators

Every acquisition High Tide closes tightens the competitive environment for independent cannabis retailers and smaller multi-store operators in Canada. That's not a complaint - it's the reality of how adult-use retail matures in any licensed market. Larger operators command better wholesale terms, carry more SKUs, invest more in point-of-sale systems and compliance infrastructure, and can absorb the per-store overhead of regulatory compliance across multiple provincial frameworks.

For independent operators, the response isn't complicated, even if it's not easy: differentiate on service, local knowledge, and product curation; keep compliance costs lean; and run the back-of-house operation - seed-to-sale tracking, compliant packaging verification, staff training on age restriction enforcement - tightly enough that regulatory exposure stays minimal. A multi-unit operator acquiring your neighboring stores at 4.5x EBITDA is also, in a sense, establishing what your business might be worth if you built it well enough to sell. That's a real data point for any cannabis retail owner thinking about a five-year exit horizon. High Tide's reported results and acquisition pricing just gave the Canadian market a fresh valuation benchmark.